ACCG100 Lecture Notes - Lecture 3: Alore, Accounting Equation, Accrual

11 May 2018

School

Department

Course

Professor

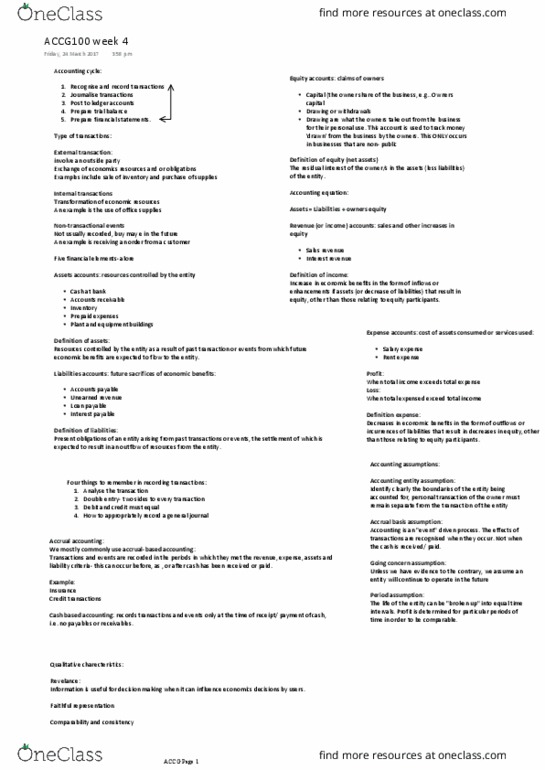

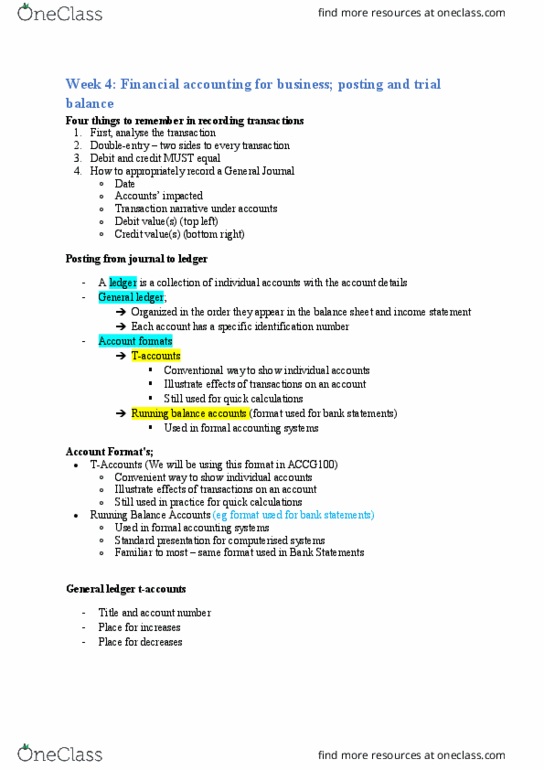

Recognise and record transactions Journalise transaction Post to ledger accounts

Financial Accounting for Business: Accounting Cycle and Double-Entry Accounting

The Accounting Cycle

Transaction records are important and necessary as they allow the creation of financial statements. Failing

to have records leads to a misstatement of assets, liabilities, revenues, expenses and equity.

Most sizable businesses use computerised accounting systems, which handles the recording process, from

initial data entry to preparation of the financial statements. But, accounting information systems vary widely

and are shaped by:

• the nature of the business,

• the types of transactions

• the size of the business,

• the volume of data

• ad uses ifoatio deads

These accounting systems are continually updated and improved to provide accurate and timely data for

decision making, and allow businesses to remain competitive. Continual developments in technology allow

for greater speed and efficiency in sharing information

Although it is possible to enter transaction information directly into the accounts, few businesses do so.

Practically every business uses these three basic steps in the recording process:

1. Analyse each transaction in terms of its effect on the accounts: only transactions that have an effect

on the assets, liabilities or equity items of a business are recorded. Evidence of external transactions

comes in a source document to support entries in accounting records. E.g. a purchase order, a

purchase invoice, a cheque, cash register tape or a sales invoice. Each source document is analysed

to determine the effect of the transaction on specific accounts. This is an important element in the

control system.

2. Enter the transaction information in a journal.

3. Transfer the journal information to the appropriate accounts in the ledger.

Transactions

External Transactions

• Involve an outside party

• Exchange of economic resources and/or obligations

Internal Transactions

• Transformation of economic resources

• An example is the use of office supplies

Non-Transactional Events

• Not usually recorded, but may be in the future, e.g. receiving an order from a customer

Common Accounts used in Recording (ALORE)

(A) Asset Accounts: resources controlled by entity (produce economic benefit for the entity itself)

• Cash at bank, (coins, notes and bank accounts)

• Accounts receivable (money to be receivable in the future, e.g. interest from bank account)

• Inventory (stocks held to be sold later – purpose of reselling them, service providers might not have

inventory – not every business has inventory)

• Prepaid expenses (e.g. insurance, opal cards, paid for, but not having enjoyed the benefit yet)

find more resources at oneclass.com

find more resources at oneclass.com

Recognise and record transactions Journalise transaction Post to ledger accounts

• Land

• Buildings

• Plant and equipment

(L) Liability Accounts: future sacrifices of economic benefits

• Accounts payable (money to be paid to other businesses in the future, e.g. loans)

• Unearned revenue/revenue received in advance (services owed if payment is made in account by

customers) (accrued expenses?)

• Loan payable

• Mortgage payable

• Interest payable

(o) Equity Accounts: claims of owners – oes euit

• Capital (the owner share of the business)

• Drawings or Withdrawals (contra equity)– what the owner(s) take for their personal use.

• share capital

• retained earnings – Retained Earnings = Balance + profits / losses – dividends.

• dividends - Dividends result in a reduction of the shareholders' claims on retained earnings.

• revenues and expenses.

(R) Revenue (or income) Accounts: sales and other increases in equity

• Sales revenue

• Interest revenue

(E) Expense Accounts: cost of assets consumed or services used

• Salary expense

• Electricity expense

• Rent expense

Double Entry Accounting

The universally used double-entry system records every transaction in appropriate accounts, where at least

two accounts are affected by each transaction to balance the accounting equation. In the T-account form,

having increases on one side and decreases on the other side reduces recording errors and helps in

determining the side totals as well as the balance. This system is logical, efficient, and ensures accuracy.

An account consists of three parts:

(1) the name of the account,

(2) On the left, a debit side (Dr)

(3) On the right, a credit side (Cr)

The accounting equation must always balance. Therefore, each transaction has a dual (double-sided) effect

on the equation, affecting TWO or more accounts. E.g. if an asset is increased, there must be a:

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Financial accounting for business: accounting cycle and double-entry accounting. Transaction records are important and necessary as they allow the creation of financial statements. Failing to have records leads to a misstatement of assets, liabilities, revenues, expenses and equity. Most sizable businesses use computerised accounting systems, which handles the recording process, from initial data entry to preparation of the financial statements. But, accounting information systems vary widely and are shaped by: the nature of the business, the types of transactions the size of the business, the volume of data: a(cid:374)d use(cid:396)s(cid:859) i(cid:374)fo(cid:396)(cid:373)atio(cid:374) de(cid:373)a(cid:374)ds. These accounting systems are continually updated and improved to provide accurate and timely data for decision making, and allow businesses to remain competitive. Continual developments in technology allow for greater speed and efficiency in sharing information. Although it is possible to enter transaction information directly into the accounts, few businesses do so. Evidence of external transactions comes in a source document to support entries in accounting records.