BU1002 Lecture Notes - Lecture 6: Cash Flow Statement, Cash Flow, Financial Statement

14 Jun 2018

School

Department

Course

Professor

Lecture 6: Statement of Cash Flows

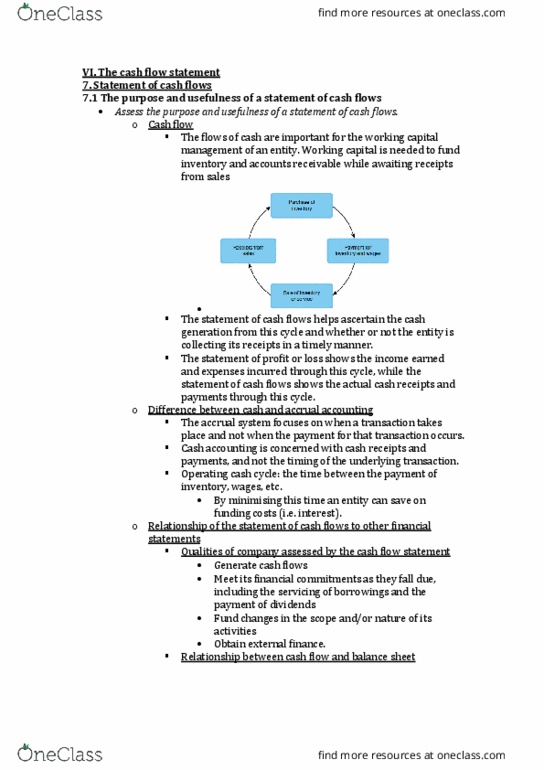

Introduction to Cash Flow Statements

- Reports information regarding cash inflows and cash outflows for a particular period

of time

- Prepared on a cash basis not an actual basis

- The statement of cash flows helps ascertain the cash flows helps ascertain the cash

geeratio fro the operatig yle ad whether or ot the etity is olletig it’s

recepts in a timely manner

Cash operating cycle

- The number of times an entity can cycle through this process generally the more

profit it can make (as long as prices are set appropriately).

- There is normally an outflow for inventory and waves before a sale is made

- Cash Flow Statement helps to determine if cash is collected in timely manner!

Remember; difference between cash and accrual accounting

- The accrual system is the basis of the income statement and focuses on when a

transaction takes place regardless of the receipt or cash

- In contrast, the statement of cash flows is concerned with cash receipts and

payments, and not the timing of underlying transaction

Why we have a statement of cash flows in an accrual reporting system

- To provide information about

o Cash receipts

o Cash payments

o Net change in cash resulting from operating, investing and financing activates

- To ensure that an entity has enough cash on hand to meet its financial commitments

in a timely fashion

The financial statements comprise

1. The income statement

2. The balance sheet

3. The statement of cash flows

4. The statement of changes in equity

- First 3 statements only show part of the activities in business

Relationship of the Statement of Cash Flows to other financial statements

- Cash flow statement gives additional information to assist decision makers in

aessig a etity’s aility to:

o Generate cash flows

o Meet financial commitments as they fall due

o Fund changes in scope and / or in nature of activites

o Obtain external finance

- Classified into three main sections reflecting the major cash flow activites

o Operating activities

o Investing activities

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Reports information regarding cash inflows and cash outflows for a particular period of time. Prepared on a cash basis not an actual basis. The statement of cash flows helps ascertain the cash flows helps ascertain the cash ge(cid:374)eratio(cid:374) fro(cid:373) the operati(cid:374)g (cid:272)y(cid:272)le a(cid:374)d whether or (cid:374)ot the e(cid:374)tity is (cid:272)olle(cid:272)ti(cid:374)g it"s recepts in a timely manner. The number of times an entity can cycle through this process generally the more profit it can make (as long as prices are set appropriately). There is normally an outflow for inventory and waves before a sale is made. Cash flow statement helps to determine if cash is collected in timely manner! The accrual system is the basis of the income statement and focuses on when a transaction takes place regardless of the receipt or cash. In contrast, the statement of cash flows is concerned with cash receipts and payments, and not the timing of underlying transaction.