1203AFE Lecture Notes - Lecture 1: Interest Rate Risk, Friendly Society, General Insurance

30 May 2018

School

Department

Course

Professor

Week 1 Money, Banking and Finance Lecture notes

Introduction

The role of the financial system

• The financial system consists of financial markets, institutions and money

• The roles of the financial system are:

o 1. To facilitate the flow of funds

o 2. To provide the mechanism to settle transactions

o 3. To generate and disseminate information

o 4. To provide the means to transfer and manage risk

o 5. To provide ways of dealing with incentive problems

Money

• Money= Means of exchange

• Barter→ coins → paper → cashless

• Ho ell this happes= futio of effiie

• The financial system (i.e. financial markets, institutions and money) allowed the

efficient allocation of funds throughout the economy

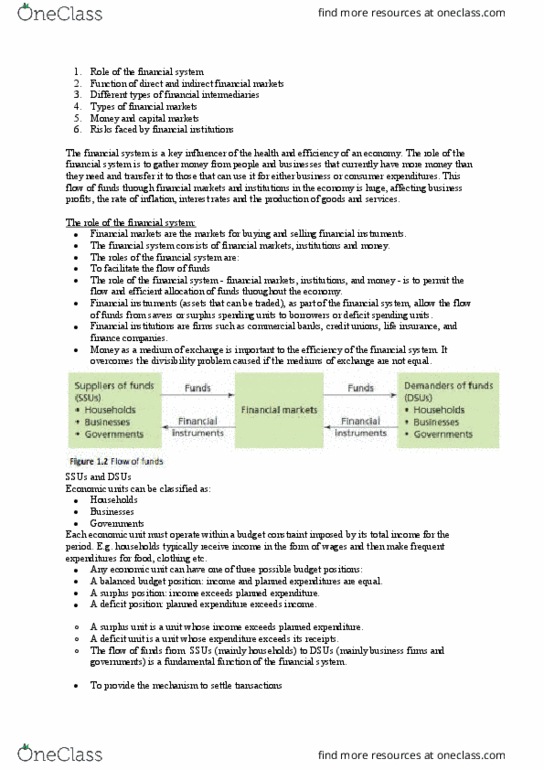

The flow of funds

• The financial system allows the flow of funds from surplus spending units (SSUs) to

deficit spending units (DSUs)

• Economic units can be classified as:

o Households

o Businesses

o Governments

• A surplus unit is a unit whose income exceeds planned expenditure

• A deficit unit is a unit whose expenditure exceeds it receipts

• The financial system is concerned with funneling money from SSUs to DSUs

• The efficient flow of funds through the economy from savers to investors and

spenders creates wealth and provides information

find more resources at oneclass.com

find more resources at oneclass.com

Maagig ‘isks ad Ietie proles

• The financial system has a role to play in managing a variety of risks and incentive

problems

• Information Asymmetry: when one party in a transaction has more information than

the other party (e.g. car seller knows more about the condition of the car than the

buyer)

• Adverse Selection: a market process which produces a sub-optimal outcome due to

parties having asymmetric information (e.g. people with dangerous jobs or high risk

lifestyles tend to purchase life insurance)

• Moral Hazard: the tendency of people and/or organizations to change their behavior

oe the eoe part to a otrat. e.g. oure driig eoes riskier he ou

have insured your car versus an uninsured car)

Financial market efficiency

• Allocational efficiency:

o fuds are alloated to their highest-alue use

o funds are allocated to projects with the highest risk-adjusted returns which

promote economic growth

• informational efficiency: (ability to obtain accurate information)

o here arket pries reflet all releat iforatio aout seurities

o allows households and firms to make intelligent decisions

• operational efficiency: (we want to transact at lower cost)

o here the osts of odutig, trasatios are as lo as possile

o society is better off, economy grows, employment grows

Trasferrig Fuds fro SSUs to DSUs

• the two methods of financing are:

o Direct financing and

o Indirect financing

Direct Financing

• SSUs lend money to DSUs and accept a financial claim (an IOU) in return

• In direct financing, this exchange takes place directly

• That is to say, in the absence of a financial intermediary (banks, credits unions etc.)

find more resources at oneclass.com

find more resources at oneclass.com

Indirect Financing

• Indirect financing:

o Direct financing requires DSUs to find SSUs that want direct claims

o This problem is resolved through the involvement of a financial intermediary

o Financial intermediaries purchase direct claims from DSUs, transform them

into direct claims and sell them to SSUs

Benefits of Financial Intermediation

• When intermediaries transform direct claims into indirect ones, they perform five

services:

o Denomination divisibility

o Currency transformation

o Maturity flexibility

o Credit risk diversification

o Liquidity

Types of Financial Intermediaries

• Australian financial intermediaries include:

o Banks, building societies and credit unions

o Foreign bank representatives

o General and life insurers

o Friendly societies

o Money market corporations, finance companies and securities

o Approved trustees

o Superannuation entities

find more resources at oneclass.com

find more resources at oneclass.com