1102AFE Lecture Notes - Lecture 3: Accounting Software, Accounts Payable, Accounting Equation

Document Summary

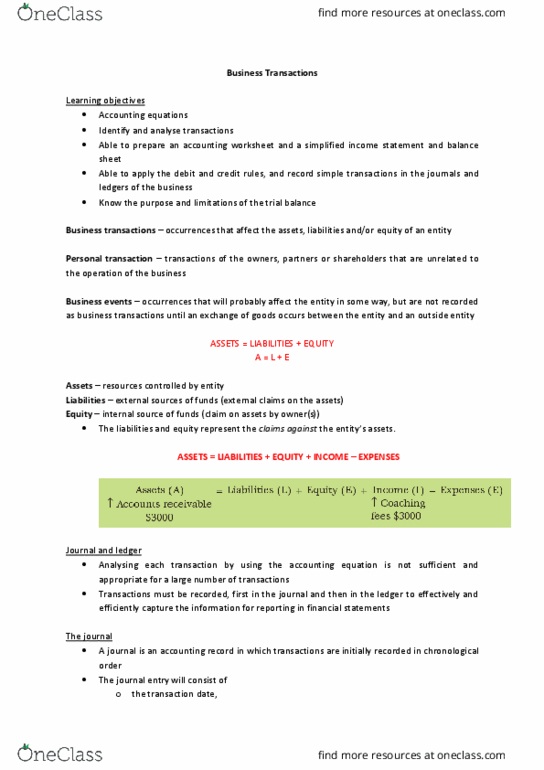

Distinguish between a personal transaction and business event. Brief overview of the components of an accounting. Occurrences that affect assets, lia(cid:271)ilities a(cid:374)d ow(cid:374)e(cid:396)s" e(cid:395)uity ite(cid:373)s. Transactions are recorded when they can be reliably measured in monetary terms. E. g. withdraws items (cash, other assets) from the business for personal use, or contributes additional funds (cash or assets from their personal funds) into the business. Transactions of owners, partners or shareholders that are unrelated to operation of business. E. g. owner uses personal funds to buy a laptop for personal use. Occurrences that have to potential to affect the entity in some way, but are not recorded as business transactions until an exchange of goods occurs between the entity and an outside party. Assets are financed in 2 ways: outside funds (liabilities) or by owners (inside funds. Lia(cid:271)ilities a(cid:374)d e(cid:395)uity (cid:396)ep(cid:396)ese(cid:374)t (cid:272)lai(cid:373)s agai(cid:374)st the e(cid:374)tity"s assets or equity) Every business transaction has at least a dual effect.