BUSN1001 Lecture Notes - Lecture 5: Deferral, Unearned Income, Ibm General Parallel File System

Document Summary

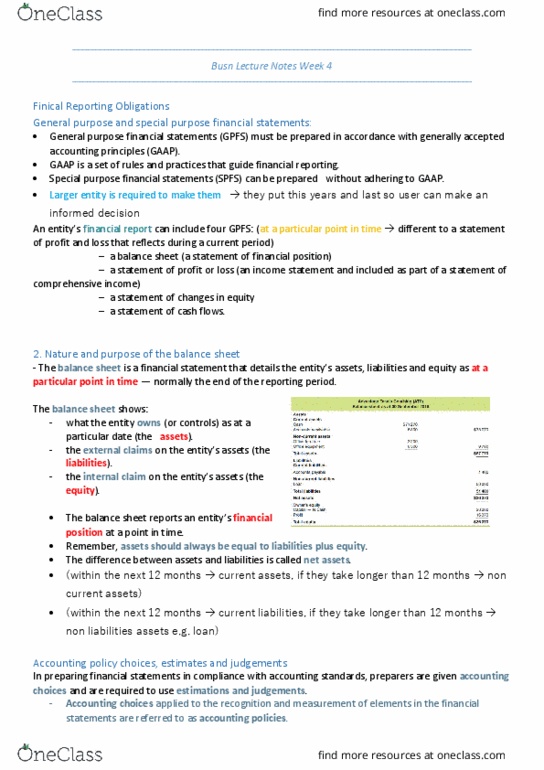

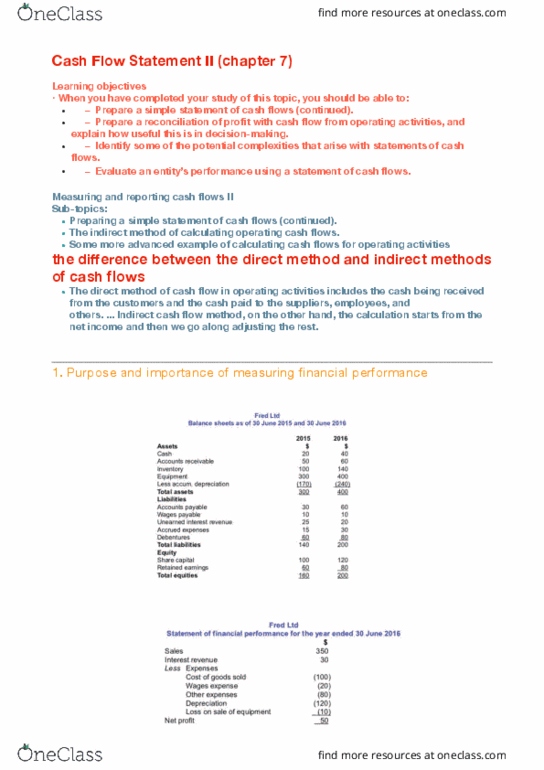

Income statement and statement of changes in equity (chapter: purpose and importance of measuring financial performance, the statement of pro t or loss re ects the accounting return for an entity over a speci ed time period. This is referred to as triple bottom line reporting: accounting concepts for financial reporting, the reporting period: period of time to which the nancial statements relates. The income has been earned (service provided), but not yet paid for (e. g. sale of goods on credit): cash is received but income is not recognised (income received in advance). Must be recognised as a liability, until the income is earned (e. g. receipt of rent from a tenant that paid in advance): accrual accounting versus cash accounting: Under accrual accounting, the following may occur for expenses: (accrual account can be recognised but not under cash accounting: expense is recognised without payment of cash (accrued expense).