BUSI 601 Chapter Notes - Chapter 4: Cost Driver

12 Sep 2016

School

Department

Course

Professor

Document Summary

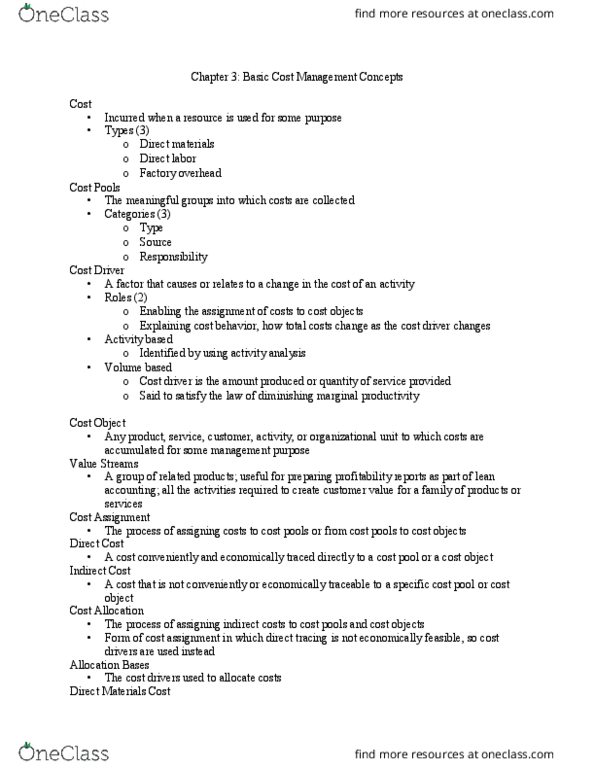

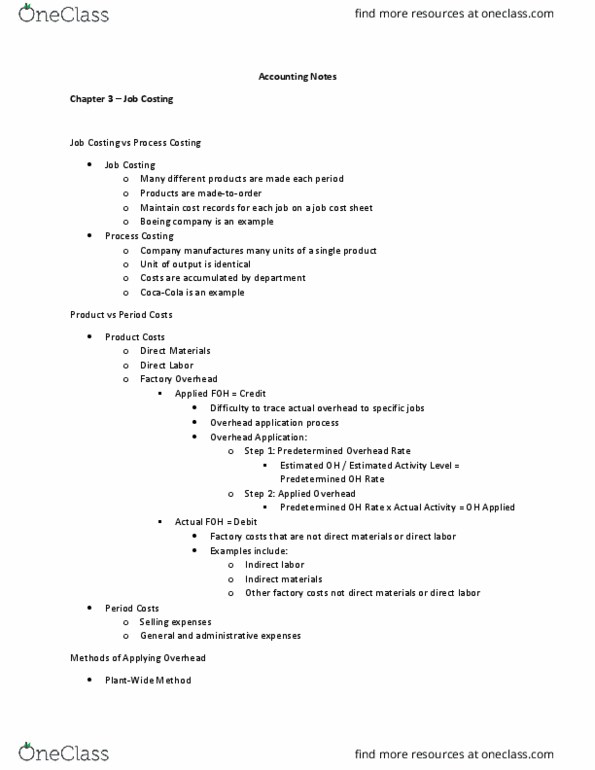

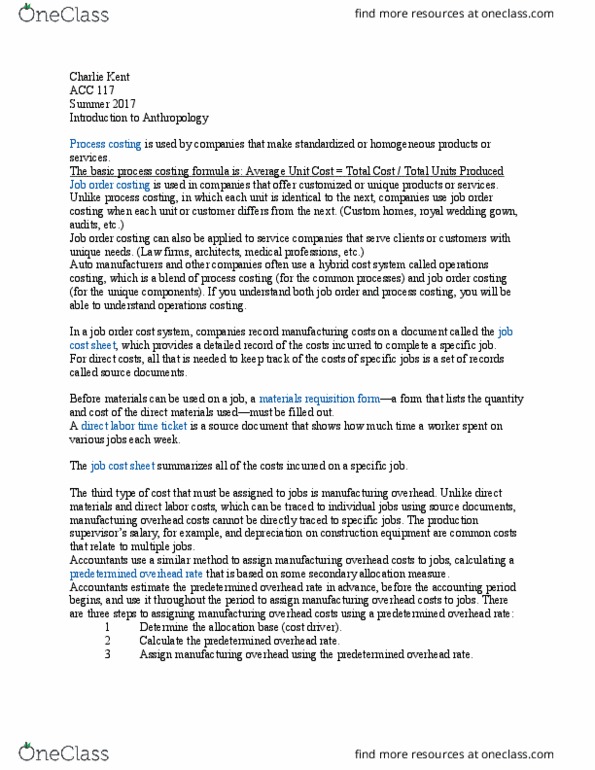

Costing: the process of accumulating, classifying, and assigning direct materials, direct labor, and factory overhead costs to products, services, or projects. Characteristics of costing method (3: cost accumulation method, cost measurement method, overhead application method. Normal costing system: uses actual costs for direct materials. Standard costing system: uses standard costs and quantities for all three types of manufacturing costs. Job costing: a product costing system that accumulates and assigns costs to specific jobs, customers, projects, or contracts. Job cost sheet: a cost sheet that records and summarizes the costs of direct materials, direct labor, and factory overhead for a particular job. Materials requisition: an online data entry or a source document used to request the release of materials into the production process. Time ticket: a sheet showing the time an employee worked on each job, the pay rate, and the total cost chargeable to each job. Overhead application: a process of allocating overhead costs to cost objects.