MLC301 Lecture Notes - Lecture 10: Indirect Tax, Double Taxation, Fringe Benefits Tax

Document Summary

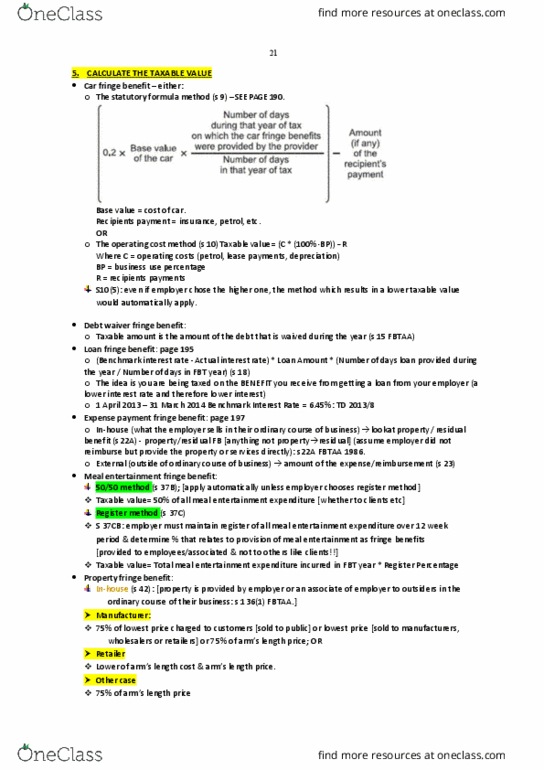

Week 10: topic 7 fbt and gst: A fb is a benefit other than a salary or wage, derived from employment. An employer can provide a range of possible benefits to an employer. E. g. car, low interest personal or housing loans, payment of expenses such as phone, electricity, school fees, subsidies rental and family holidays. An employer is liable for the tax on the total (cid:448)alue of the grossed up (cid:448)alue of fb(cid:859)s pro(cid:448)ided to employees or associates of employees. The fb is not assessable to the employee (s23l itaa 36). = employer: general operation of scheme, determine the type of fb, calculate the taxable value of the benefits and the fbt liability. Calculations: not required to do any calculations (multiply (cid:858)gross-up-rate(cid:859) (cid:449)ith the fb. Then multiply the benefit by the tax rate) Reduction is allowed if the fb provided to the employee would have been an allowable deduction if the employee had incurred the expense.