MLC301 Lecture Notes - Lecture 6: Kurt Nilsen

Document Summary

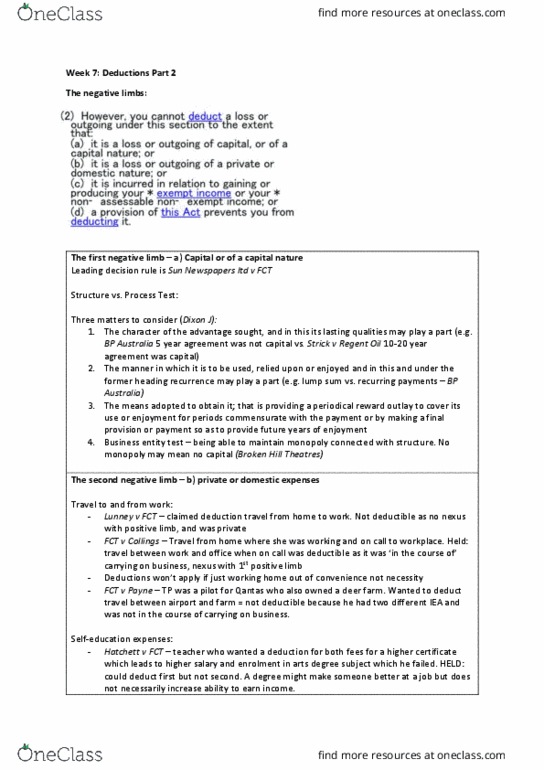

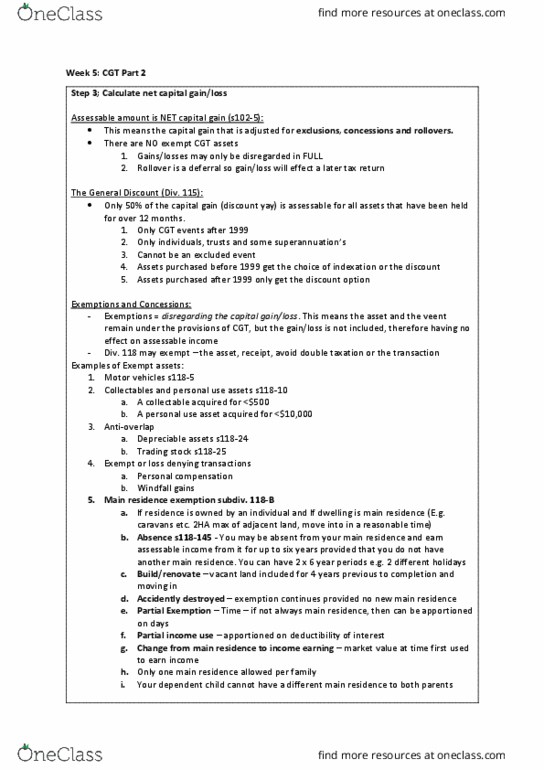

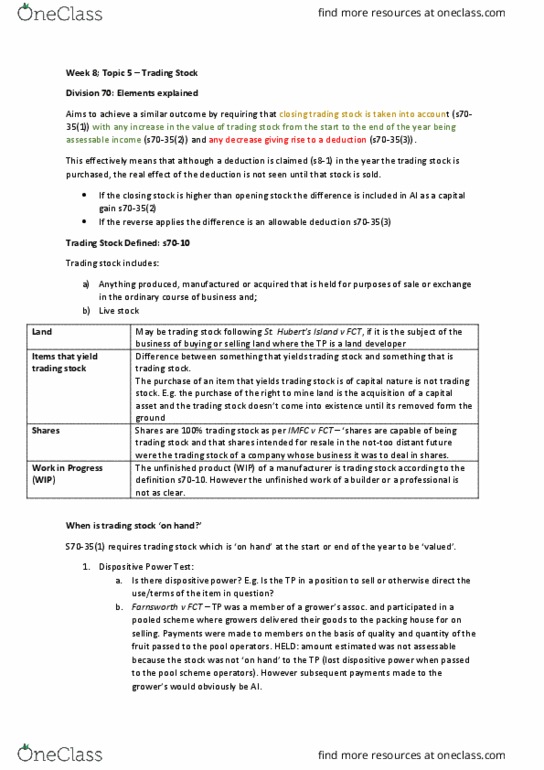

You must prove either a) or b) from the positive limb (1): Incurred in gaining or producing your assessable income. It is necessarily incurred in carrying on a business for the purpose of gaining or producing your assessable income. You must not be able to prove any of the 4 negative limbs (2): It is a loss or outgoing of capital, or of a capital nature. It is a loss or outgoing of a private or domestic nature. It is incurred in relation to gaining or producing your exempt income on your non-assessable non-exempt income: a provision from this act prevents you from deducting it. Nexus with income: to establish a sufficient nedxus between the loss or outgoing and the assessable income we use either the: Incidental and relevant test: herald and weekly times v fct - expenditure was wholly and exclusively laid out for the production of income and was deductible.