MAF307 Lecture Notes - Lecture 10: Capital Asset Pricing Model, Investment Fund, Sharpe Ratio

Document Summary

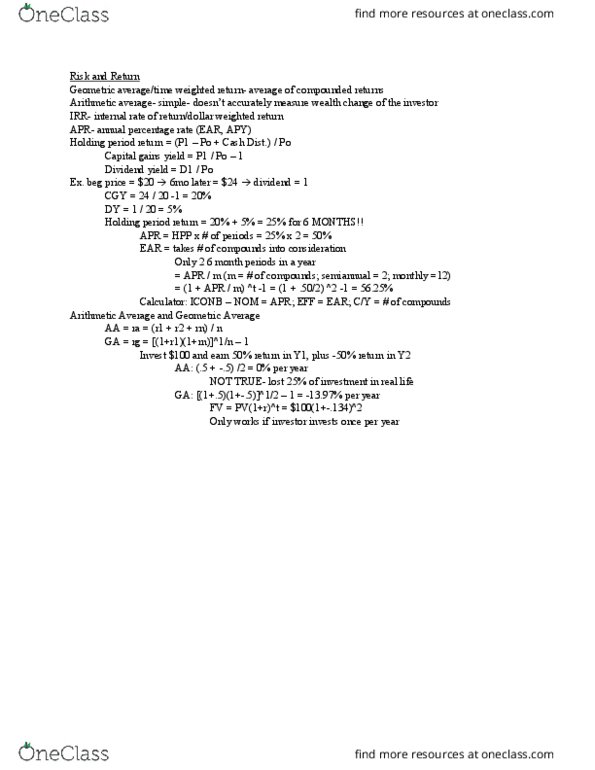

Fund managers prefer this over dollar weighted returns. Internal rate of return considering the cash flow to or from an investment. Returns are weighted by the amount invested in each stock. Stock pays a dividend of per share. How should we average returns: arithmetic mean: normal (preferred when forecasting returns, geometric mean: (preferred when averaging historical data) From previous example, geometric mean = [ (1. 1) (1. 0566) ]1/2 1 = 7. 81% Predicting expected returns: arithmetic mean: invested over 2 yrs. = $ 1. 5625 at the end of next 2 yrs. If expected return is r, then (1+r)2 = 1. 5625. If we estimate averages over past t number of years and wish to forecast average return for future h number of years, then. Forecasted future return = arithmetic average x (1-h/t) + geometric average x (h/t) Jensen"s alpha: a = rp - [ rf + p ( rm - rf) ] rp = average return on the portfolio.